Introduction: Hunt warned pound would suffer if he misreads the markets

Good morning, and welcome to our rolling of business, the financial markets, and the world economy.

With just over week to go until the budget, Jeremy Hunt is being warned not to risk unfunded tax cuts that could cause ructions in the financial markets.

The chancellor is understandably keen to offer some pre-election sweeteners, in the hope of closing the gap with Labour. City economists, though, warn that there may not be as much fiscal firepower to play with as Hunt would like.

ING, the Dutch banking group, estimates that the money available for tax cuts – so-called “headroom” – now equals £18bn. That’s up from £13bn in November, but lower than estimated a few weeks ago, as the City has cut it expectations for Bank of England rate cuts.

This headroom is the amount of money the chancellor can spend, and still hit his fiscal rule – to have debt falling, as a share of GDP, in five years time.

£13bn could, potentially, allow the chancellor to cut income tax by 2p in the pound – as a 1p cut to the basic rate of income tax is slated to cost roughly £7bn/year. That wouldn’t leave very much left over, though.

As ING’s developed market economist, James Smith, puts it in a research note this week:

The situation is tight. And it’s possible our estimate of headroom is too optimistic.

What about cutting spending, though, to free up money for tax cuts? ING says such spending restraint looks “unrealistic”, given the government’s current plans already imply more painful austerity for departments.

Talk of tax cuts will revive visions of the 2022 mini-budget debacle, when Kwasi Kwarteng crashed the pound and the bond markets by announcing unfunded tax cuts, without any scrutiny from the independent Office for Budget Responsibility.

The situation is different this time – the OBR will give its verdict as soon as Hunt sits down next Wednesday after delivering the budget.

Smith says that funding tax cuts today with unrealised and potentially challenging spending cuts tomorrow may “raise a few eyebrows among investors”, but in reality this wouldn’t be a new approach.

Smith told The Guardian:

“The savings earmarked so far are already very challenging and further savings appear unrealistic.

Talk of tax cuts inevitably triggers memories of the 2022 mini budget crisis, where UK government borrowing costs rose precipitously following a package of unfunded measures designed to boost growth.”

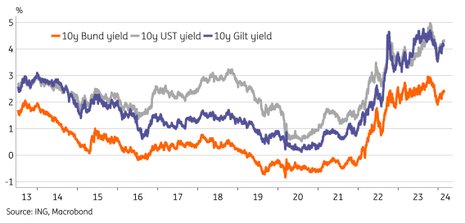

He warns, though, that fresh tax cuts could still apply some upward pressure on yields – the measure of Britain’s borrowing costs.

ING’s gauge of risk premium in the government bond market suggests investors are still keeping an eye on UK fiscal risk – with UK borrowing costs higher than Germany’s, but in line with the US.

Sizable cuts to income tax would add further impetus for the Bank of England to keep interest rates on hold a little longer, ING predicts, meaning more pain for borrowers and a delay to rate cuts.

ING reports that market conditions in the currency market are calm, which should please Hunt.

They say:

When it comes to FX markets, current market conditions could not be more different than those that prevailed at the height of the Liz Truss debacle.

But, they warn that if the chancellor was to “misread the mood of gilt investors and cause another upset”, sterling would take a hit.

ING add:

Short-term models suggest a 2% sell-off in sterling could happen quite easily were investors to again demand a risk premium of sterling asset markets.

The Institute for Fiscal Studies are pointing out this morning that UK taxes are heading to record-high levels, as a share of national income.

They warn that the public finances face an ‘unhappy outlook’, with debt high and rising, and barely on track to start falling in five year’s time.

In a warning shot to Hunt, they say:

Unless the Chancellor is willing to spell out where the cuts will fall, the temptation to scale back provisional spending plans further to ‘pay for’ new tax cuts should be avoided.

We’ll hear more from the IFS this morning, as they present their analysis of Hunt’s options ahead of the budget.

The agenda

-

8am GMT: Kantar’s latest UK supermarket sales and market share data

-

10am GMT: Institute for Fiscal Studies presents Spring Budget 2024: the Chancellor’s options

-

1.30pm GMT: US durable goods orders for January

-

1.40pm GMT: Bank of England deputy governor Dave Ramsden gives keynote address at Association for Financial Markets in Europe’s Bond Trading, Innovation and Evolution Forum

Key events

Shein ‘considering London rather than New York IPO amid US scrutiny’

Julia Kollewe

The fast-fashion company Shein is reportedly considering a stock market flotation in London rather than New York because of potential problems with a listing in the US, its preferred location.

And Jeremy Hunt is said to be keen to persuade Shein to pick the City over Wall Street:

EXCLUSIVE: Jeremy Hunt, the chancellor, has met Shein chairman Donald Tang in a bid to persuade the Singapore-based online fashion giant to pursue one of London’s biggest-ever IPOs – a possibility I revealed in a previous story on @SkyNews in December. https://t.co/ubFGi8q2rz

— Mark Kleinman (@MarkKleinmanSky) February 27, 2024

Shein, which was founded in China but is based in Singapore, is in the early stages of exploring an initial public offering in London because it believes it is unlikely that the US Securities and Exchange Commission would approve its initial public offering (IPO), Bloomberg reported.

A UK listing would be a potential boost to the country’s standing as a global financial centre, after a number of companies snubbed the London stock exchange in favour of the Nasdaq in New York, despite the government’s efforts to persuade more firms to list there.

More here:

In the City, shares in Currys have jumped 3% as the battle to take control of the electricals goods retailer takes another twist.

Sky News reports that Elliott Advisors has improved its existing bid for Currys, slightly.

Elliott’s revised proposal valued Currys at between 65p and 70p-a-share, compared with an initial 62p-a-share bid worth £700m, they say. More here.

Currys rejected that earlier approach from Elliott earlier this month, while its share soared last week after Chinese e-commerce company JD.com said it was considering a bid.

The IFS’s pre-budget briefing ended with a discussion about the UK’s child benefit rules, under which payments are tapered if a parent earns over £50,000 per year, and cut off at £60,000.

This system, introduced by chancellor George Osborne in 2012, is criticised – as it doesn’t capture a household’s income (two parents earning £49,999 each would qualify for full payments, while one on £60,000 would lose the lot).

Paul Johnson says it’s not impossible that someone could still be entitled to universal credit despite earning £50,000 (due to recent changes in eligibility).

Carl Emmerson suggest that a “rational” system would say either that a) child benefit should be universal, or b) that it should be abolished, and the money used to make the child top-up payment in universal credit more generous.

The latter option could provide a means-tested system, which isn’t currently the case.

Incidentally, the Financial Times reports this morning that Jeremy Hunt is under growing Conservative pressure to reform child benefit and remove “one of the UK’s most notorious tax cliff edges”.

However, the chancellor’s allies said Budget measures on this issue were “unlikely at this stage” but had not been ruled out.

Q: Why is the UK’s GDP-per-capita perforrming worse than straight GDP growth, if we think immigration should push up GDP-per-capita?

IFS director Paul Johnson says we don’t necessarily think immigration will push up GDP-per-capita, although it will clearly increase national income.

It depends who is coming over to the UK, and what jobs they are going into, Johnson explains.

The current inflow of people is very bimodal, Johnson adds, with a lot of high-income, high-skill people, and also a lot at the bottom of the earnings distribution.

Reminder: UK GDP per capita hasn’t grown for the last seven quarters, a record-breakingly bad run of weak living standards.

Two quarters of contraction of real GDP will get headlines, but maybe this is the real story 👇

💥 GDP per person dropped every quarter of 2023. It hasn’t grown since Q1 2022

💥 That’s 7 quarters – longest unbroken run without per capita GDP growth since records began in 1955 pic.twitter.com/bknjT5TlMy— Andy Bruce (@BruceReuters) February 15, 2024

Q: Would above-inflation pay increases for the public and private sectors boost the economy and lift growth?

IFS deputy director Carl Emmerson says stronger private sector wage growth would create more pressure to raise public sector pay.

That extra cash in the economy, if it’s not associated with increased productivity, is inflation – if people are being paid more to produce the same as before.

That could prompt the Bank of England to keep interest rates higher for longer, Emmerson says.

So while it would produce some growth, it wouldn’t be stable growth, he argues.

IFS director Paul Johnson points out that pay growth has been “unbelievably bad” in the last 15 years, with median pay barely higher than 15 years ago.

Q: Is there a case for increasing borrowing now, in the short-run, to prime the pump so the economy grows faster in the long run – bringing down the debt and the deficit in the long term?

The IFS’s Carl Emmerson says the risk of cutting taxes or increasing spending now, to lift growth, is that the Bank of England would say “hang on, we’re worried about that injection of cash into the economy”.

If the Bank doesn’t see spare capacity in the economy, they could raise interest rates or simply lower them less quickly in response.

The argument is different for long-term investment. There may well be investments which could be done well, and deliver a return above the long-term cost of borrowing.

Emmerson points out that the UK has been able to borrow at low costs in recent global crises (such as Covid-19); the danger is a UK-specific crisis which prompts international investors to demand a higher rate of return when lending to us.

Q: Why are there differences between the OBR and Bank of England growth forecasts? (see earlier post). Have they explained why they disagree?

The IFS’s Carl Emmerson says the OBR provides more information about its forecasts than the BoE, which doesn’t really give much insight into what’s behind its projections.

He points out that the BoE has been more pessimistic about the impact of Brexit, which may explain why it forecasts slower growth than the OBR.

Or it could be because the BoE forecasts are trying to reflect the collective view of the members of the Monetary Policy Committee (the nine policymakers who set interest rates).

Q: Do fiscal pressures mean the State need to stop doing some things?

IFS director Paul Johnson says the UK has a decision to make – it can keep providing the current public services, if people accept that taxes will remain at their current levels, and possibly rise higher over time.

The UK has been struggling to avoid this for a long time, Johnson adds – pointing out that in other countries the tax burden rose in the 1970s, 80s and 90s, while the UK’s didn’t.

We’re sort of catching up with them, although we haven’t broadly caught up with the rest of Western Europe.

Some state commitments have been dropped since the 70s, Johnson points out – we’re not subsidising nationalised industries, or building public housing, while there’s a lot more private finance in higher education.

Defence spending has been “dramatically cut”, Johnson adds. But that’s now likely to rise in the next few years.

It’s hard to see where further deep spending cuts can be made, Johnson adds, given how many public sectors – such as local government, justice, prisons and social care – are already struggling.

My guess is that we’re more likely to end up with higher taxes than we are with the state withdrawing from some provision.

But that is a conversation we ought to be having, and we’re not.

The IFS are now taking questions about next week’s budget.

Q: Are the current fiscal rules sensible? How realistic is it to be able to predict the size of the economy, and the difference between two large numbers, five years into the future.

(this refers to the goal of showing debt falling as a share of GDP in five years time).

IFS’s Carl Emmerson says it’s sensible to have forward-looking fiscal targets.

He says the chancellor has another fiscal rule, to be on course to be raising enough revenue to pay for spending in three years time.

That’s good, as it gives flexibility if the economy suffers a shock.

But it still allows a chancellor to “pretend” to have plans to raise taxes or to cut spending, to hit a target in future.

Emmerson adds that there is always huge uncertainty over what the economy will be like in five years time; chancellors should look at the ‘central forecasts’, and build in some margin for error in case of shocks.

He adds:

The forecasts we have are the best guide to the future that we have.

What if Jeremy Hunt decides to ignore the IFS’s advice, and decides to cut taxes next week?

IFS deputy director Carl Emmerson says there are more growth-friendly options than cutting income tax or national insurance.

Cutting stamp duty on property purchases, or on shares, would be more growth-friendly, Emmerson says.

IFS: Chancellor should hold off from fresh tax cuts until spending review

UK borrowing in 2023–24 is now on course to be £113bn, the IFS estimate, which is £11bn less than forecast by the OBR in November.

But it’s still a high amount, the IFS point out today – and “much bigger than forecast two years ago”.

Debt is “barely on a downward trajectory” in five years time, despite the forecasts being predicated on unspecified cuts to public spending after the election.

The IFS’s Carl Emmerson says:

Clearly the risk here is that whoever is chancellor after the election might be unable or unwilling to deliver on those spending plans.

Therefore, the IFS thinks any fresh tax cuts should be delayed until a detailed Spending Review has been held, rather than implementing further tax cuts now that are “paid for” by uncertain spending cuts in the next parliament.

The UK’s growth prospects will determine how much wiggle-room the chancellor has for tax cuts or spending increases, while still having debt falling in five years.

The IFS point out that the Bank of England’s growth forecasts are rather less optimistic than those of the Office for Budget Responsibility – the independent group who will give their assessment of the budget.

Carl Emmerson, deputy director of the IFS, runs through the context for the budget on 6 March.

Emmerson points out that UK GDP growth has been “abysmal”, with GDP per head still not above its level in 2019.

The backdrop here is a terrible period of growth going back to 2008.

That period covers the great recession after the financial crisis, the very weak recovery afterwards, the Covid-19 pandemic and lockdowns, and the recent stagnation over the last couple of years – culminating in the current technical recession, Emmerson says.